How Is Net Worth Calculated? A Complete Guide for Beginners

Understanding your net worth is one of the most important steps in taking control of your financial future. Whether you're just starting your career, planning for retirement, or want to get a clear picture of your financial health, knowing how to calculate net worth gives you a powerful snapshot of where you stand financially.

In this comprehensive guide, we'll walk you through everything you need to know about net worth calculation, from the basic formula to practical examples and tips for improving your financial position.

What Is Net Worth?

Net worth is the total value of everything you own minus everything you owe. It's essentially a measure of your financial health at a specific point in time. Think of it as your personal balance sheet that shows whether you're building wealth or falling behind financially.

Your net worth can be positive or negative. A positive net worth means you own more than you owe, while a negative net worth means your debts exceed your assets. Many young professionals starting their careers have negative net worth due to student loans, but this typically improves over time with smart financial planning.

The Net Worth Formula: Simple but Powerful

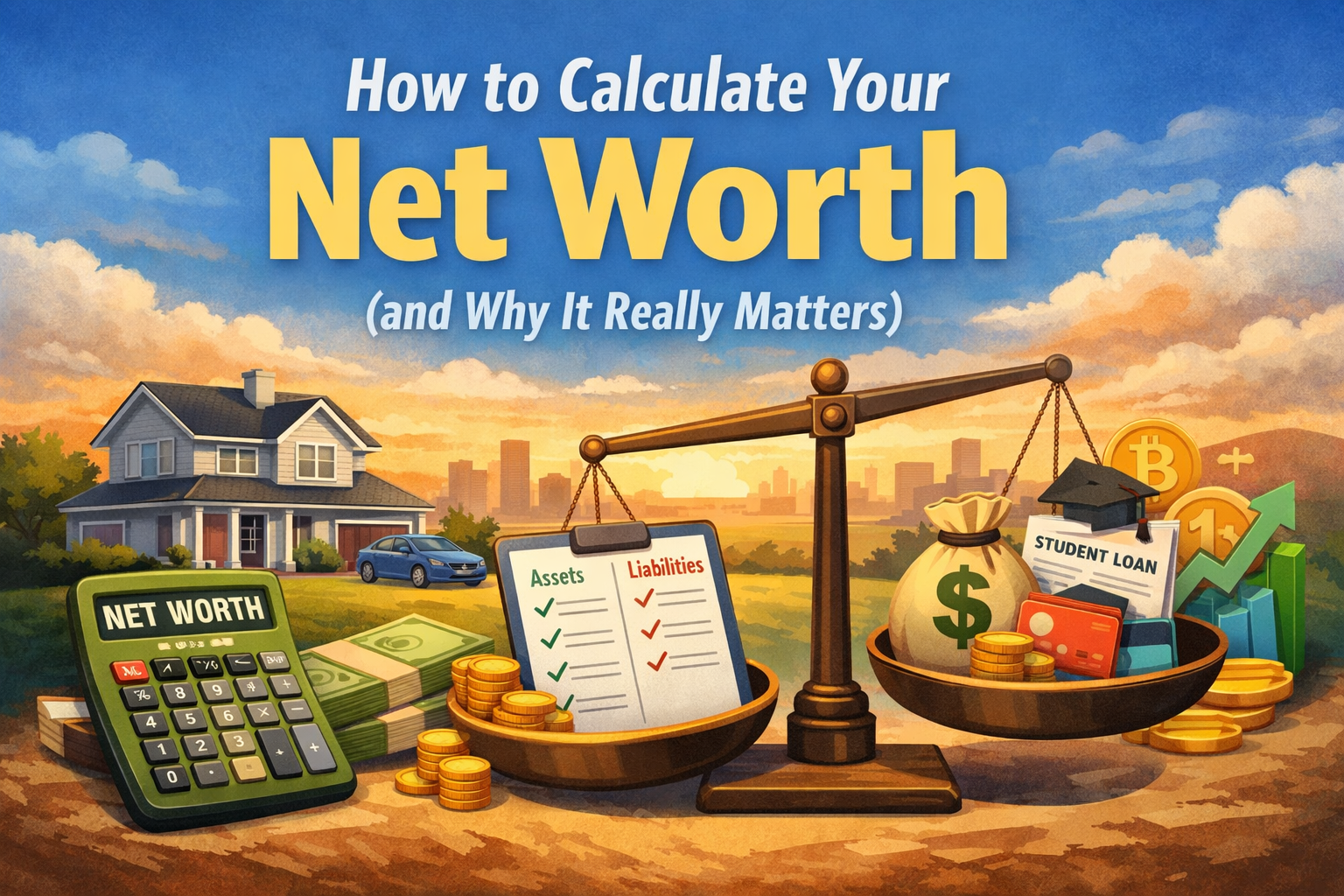

The basic formula for calculating net worth is straightforward:

Net Worth = Total Assets - Total Liabilities

While the formula itself is simple, accurately identifying and valuing your assets and liabilities requires some careful thought and organization. Let's break down each component in detail.

Understanding Assets: What You Own

Assets are anything of value that you own. They can be divided into several categories, each contributing to your overall financial picture.

Liquid Assets

Liquid assets are cash or things that can quickly be converted to cash without losing significant value. These include:

Cash and Bank Accounts: This includes checking accounts, savings accounts, and any physical cash you have on hand. These are your most liquid assets and should be easy to total up by checking your latest bank statements.

Money Market Accounts: These interest-bearing accounts typically offer higher returns than regular savings accounts while maintaining easy access to your funds.

Certificates of Deposit (CDs): While not as immediately accessible as savings accounts, CDs are still considered relatively liquid assets. Include the current value, including any accrued interest.

Investment Assets

Investment assets represent money you've put to work in the financial markets or other investment vehicles:

Retirement Accounts: Include the current balance of all retirement accounts such as 401(k)s, 403(b)s, traditional IRAs, Roth IRAs, and any pension plan values. Use the current market value, not your contribution amount.

Brokerage Accounts: Any taxable investment accounts holding stocks, bonds, mutual funds, ETFs, or other securities should be valued at their current market price.

Stocks and Bonds: Individual securities you own directly should be included at their current market value.

Cryptocurrency: If you own Bitcoin, Ethereum, or other digital currencies, include their current market value. Be aware that crypto values can be highly volatile.

Real Estate and Property

Physical property often represents the largest asset for many individuals:

Primary Residence: Include the current market value of your home. You can use recent comparable sales in your neighborhood, online valuation tools, or a professional appraisal to estimate this value.

Investment Properties: Any rental properties or vacation homes you own should be valued at their current fair market value, not what you paid for them.

Land: Undeveloped land or lots you own contribute to your net worth based on current market values.

Personal Property

While often overlooked, valuable personal property should be included:

Vehicles: Cars, motorcycles, boats, and RVs have value, though they typically depreciate over time. Use current market values from resources like Kelley Blue Book or similar valuation guides.

Jewelry and Collectibles: High-value jewelry, art, antiques, or collectibles can contribute significantly to net worth. For expensive items, consider getting professional appraisals.

Business Ownership: If you own a business or have equity in one, this should be included. Valuing a business can be complex and may require professional assistance.

Other Assets

Life Insurance Cash Value: Permanent life insurance policies, as whole life or universal li, build cash value over time. Include this amount, not the death benefit.

Valuable Personal Possessions: High-end electronics, musical instruments, or other valuable items can be included, though most financial advisors suggest focusing on major assets rather than everyday possessions.

Understanding Liabilities: What You Owe

Liabilities are all your debts and financial obligations. Being honest and comprehensive about your liabilities is crucial for an accurate net worth calculation.

Mortgage Debt

Primary Mortgage: Include the remaining principal balance on your home loan. Don't include future interest you'll pay, just the current outstanding balance.

Home Equity Loans and HELOCs: Any secondary mortgages or home equity lines of credit should be included at their current balance.

Investment Property Mortgages: Outstanding balances on loans for rental or investment properties.

Consumer Debt

Credit Card Balances: Include the current balance on all credit cards, not just the minimum payment.

Personal Loans: Any unsecured personal loans from banks, credit unions, or online lenders.

Auto Loans: The remaining balance on any car, truck, motorcycle, or other vehicle loans.

Student Loans: All education debt, whether federal or private, should be included at the current outstanding balance.

Other Liabilities

Medical Debt: Any outstanding medical bills or payment plans.

Tax Liens: Any unpaid taxes owed to federal, state, or local governments.

Other Debts: This could include money owed to family or friends, outstanding legal judgments, or any other financial obligations.

Step-by-Step: How to Calculate Your Net Worth

Now that you understand assets and liabilities, let's walk through the actual calculation process:

Step 1: List All Your Assets

Create a spreadsheet or use pen and paper to list every asset category. Go through bank statements, investment account statements, property records, and loan documents. Be thorough and don't forget smaller accounts or assets.

Step 2: Determine Current Values

For each asset, determine its current fair market value. For bank accounts and investments, this is straightforward from your statements. For property and vehicles, you may need to do research or get estimates.

Step 3: Total Your Assets

Add up all your asset values to get your total assets figure. This number represents everything you own.

Step 4: List All Your Liabilities

Make a comprehensive list of every debt you owe. Check credit card statements, loan documents, and your credit report to ensure you don't miss anything.

Step 5: Total Your Liabilities

Sum up all your debts to calculate your total liabilities. This is everything you owe.

Step 6: Calculate Your Net Worth

Subtract your total liabilities from your total assets. The result is your net worth.

Example Calculation:

Let's look at a practical example for Sarah, a 32-year-old marketing professional:

Assets:

- Checking and Savings: $15,000

- 401(k): $85,000

- Roth IRA: $25,000

- Home Value: $350,000

- Car Value: $18,000

- Personal Property: $10,000 Total Assets: $503,000

Liabilities:

- Mortgage Balance: $280,000

- Car Loan: $12,000

- Student Loans: $35,000

- Credit Card Debt: $3,000 Total Liabilities: $330,000

Net Worth = $503,000 - $330,000 = $173,000

Sarah has a positive net worth of $173,000, indicating she's building wealth despite having substantial debts.

Common Mistakes to Avoid When Calculating Net Worth

Overvaluing Assets: Be realistic about property and personal item values. Your home is worth what someone would pay for it today, not what you hope to sell it for.

Forgetting Hidden Debts: Check your credit report annually to ensure you haven't missed any outstanding debts or accounts.

Including Future Income: Net worth is a snapshot of your current financial position. Don't include your salary, expected bonuses, or potential inheritance.

Ignoring Small Accounts: That old savings account with $500 or the credit card with a $200 balance might seem insignificant, but they add up.

Using Purchase Price Instead of Current Value: Assets like homes and investments should be valued at current market prices, not what you paid for them.

Why Calculating Your Net Worth Matters

Tracking your net worth regularly provides several important benefits for your financial journey:

Financial Health Indicator: Net worth gives you a clear picture of your overall financial position beyond just your income or savings account balance.

Progress Tracking: By calculating net worth quarterly or annually, you can track whether you're moving in the right direction financially.

Goal Setting: Knowing your starting point helps you set realistic financial goals and create actionable plans to achieve them.

Retirement Planning: Understanding your net worth helps determine if you're on track for retirement and how much more you need to save.

Better Financial Decisions: Awareness of your complete financial picture leads to more informed decisions about spending, saving, and investing.

How Often Should You Calculate Net Worth?

Most financial experts recommend calculating your net worth at least once per year. Many people find quarterly calculations helpful, especially if they're actively working toward financial goals. Monthly calculations might be excessive and don't typically show meaningful changes, though some highly motivated individuals track monthly to stay accountable.

Choose a regular schedule and stick to it. Many people calculate net worth at the beginning of each year as part of their financial planning routine.

Tips for Improving Your Net Worth

Once you know your net worth, the next step is improving it. Here are proven strategies:

Pay Down High-Interest Debt: Focus on eliminating credit card debt and other high-interest loans first to reduce your liabilities faster.

Increase Your Savings Rate: Even small increases in how much you save each month compound significantly over time.

Invest Consistently: Regular contributions to retirement accounts and investment portfolios grow your assets through compound returns.

Avoid Lifestyle Inflation: As your income increases, resist the urge to proportionally increase spending. Save and invest the difference instead.

Increase Your Income: Seek promotions, develop new skills, start a side business, or find other ways to boost your earning potential.

Make Smart Purchase Decisions: Consider the long-term impact on your net worth before making major purchases or taking on new debt.

Net Worth by Age: How Do You Compare?

While everyone's financial journey is unique, knowing the average net worth by age can provide context. According to Federal Reserve data, median net worth by age group in the United States is approximately:

- Under 35: $14,000

- 35-44: $91,000

- 45-54: $168,000

- 55-64: $255,000

- 65-74: $410,000

Remember, these are medians, meaning half of households have more and half have less. Don't get discouraged if you're below these numbers, especially if you're younger or just starting your wealth-building journey.

Conclusion: Your Net Worth Journey Starts Now

Calculating your net worth might seem intimidating at first, but it's one of the most empowering financial exercises you can do. By understanding the simple formula of assets minus liabilities and taking the time to honestly assess your financial position, you create a foundation for building lasting wealth.

Remember that net worth is just a number, and a snapshot at that. What matters most is the trend over time. Are you moving in the right direction? Are your assets growing and your debts shrinking? These are the questions that truly matter.

Start by calculating your net worth today. Set up a simple spreadsheet, gather your financial documents, and work through the process. You might be pleasantly surprised by what you discover, or you might identify areas that need attention. Either way, you'll have the clarity and knowledge you need to take control of your financial future.

Your journey to financial freedom begins with understanding where you stand. Calculate your net worth today and commit to checking it regularly as you build the wealth and security you deserve.

Ready to calculate? Start here! https://networthafrica.com/calculator